KYC Guide 2023—What’s KYC and Why is It Important?

Everything you wanted to google about KYC in one article.

Whether you’re new to customer verification or experienced in customer onboarding, this page contains many useful resources to expand your KYC knowledge.

During the KYC process, businesses gather information about the customer to ensure that it’s valid throughout the business relationship

What does KYC mean?

Know Your Customer (KYC) is the process of identifying and verifying customers. Identification means gathering a customer’s personal data; verification means checking that this data is accurate.

To identify a customer, businesses usually need at least the following data:

- name;

- date of birth;

- address.

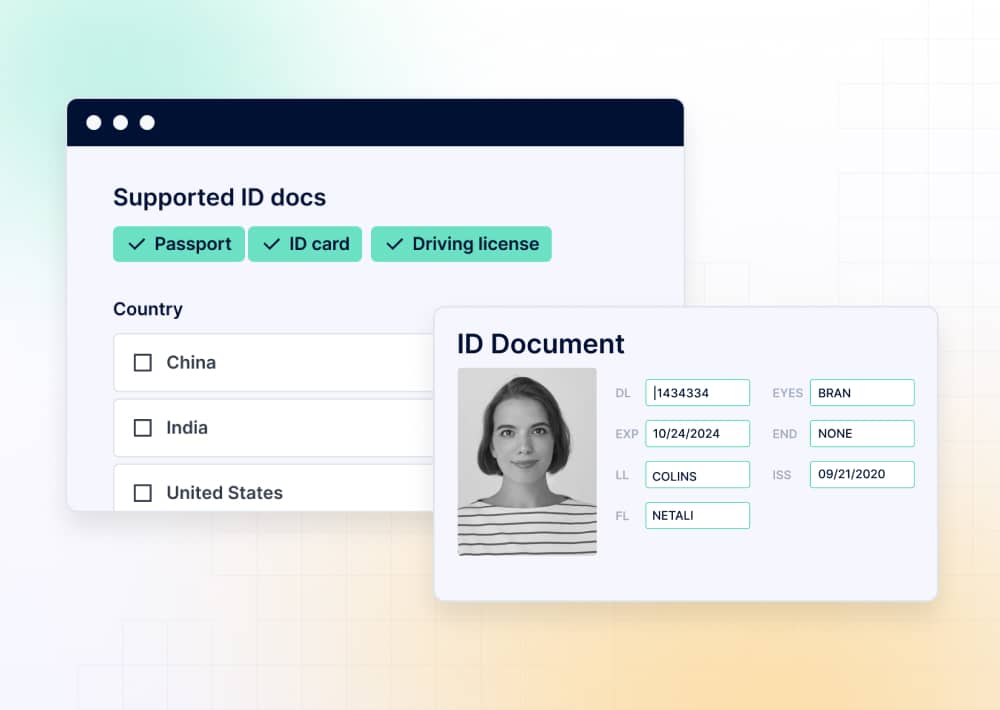

To verify this data, businesses can follow a document-based verification approach. This involves checking the customer’s identity and proof of address (usually a utility bill) documents and confirming that they are authentic and valid.

Under Anti-Money Laundering (AML) obligations, businesses must also ensure that customers are trusted individuals—i.e., not fraudsters or under sanctions. This can be done by сhecking global sanctions lists, watchlists, blocklists, or adverse media. Check out other articles from our blog that go into these processes in detail:

- Global Watchlist Screening—All Sanctions Database

- Adverse Media: How and Where to Check for Negative News

- What Is a KYC Analyst?

- KYC: Know Your Customer Compliance with High Conversion

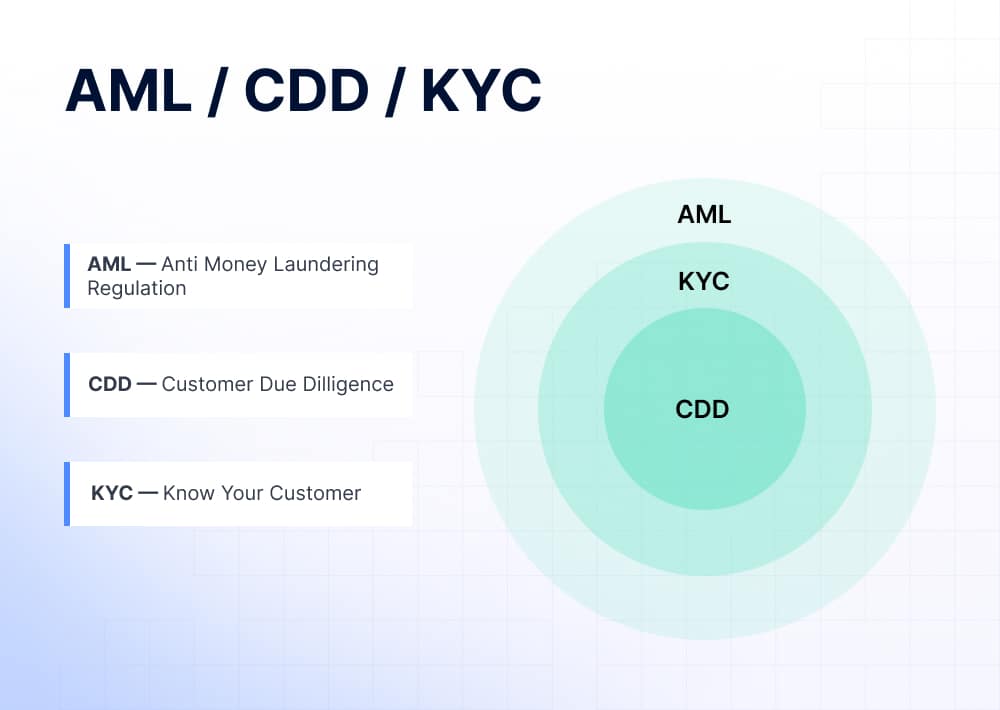

What’s the difference between KYC and AML?

KYC is actually just one of the many procedures that make up Anti-Money Laundering (AML) compliance, which covers all the measures used by financial institutions and governments to combat financial crimes. So, AML encompasses a variety of policies, controls and procedures, including AML training, detection of suspicious activity, reporting, and more.

AML compliance includes KYC, transaction monitoring, suspicious activity reporting, and other measures that businesses can implement to combat money laundering

Why is the KYC process important?

The Know Your Customer process helps detect fraud and prevent financial crimes like money laundering.

Stolen personal data can be used to register on platforms—from payment apps to dating sites—and perform illicit transactions or scam honest users. These risks obligate businesses to conduct customer verification in the form of KYC.

Failing to fulfill KYC obligations can lead to regulatory sanctions and reputational losses for AML-obligated companies. For instance, banking giant HSBC was fined £64m ($72.4m) in 2021 for weaknesses in its financial crime safeguards.

Even non-AML-obligated companies can face significant risks (multi-accounting, illegal chargebacks, etc.) if they don’t voluntarily implement KYC procedures.

Who needs KYC?

Since KYC falls within AML requirements, any AML-obligated business must perform KYC procedures. Typically, these are financial institutions, crypto businesses, and gambling platforms that offer their services on a constant and unlimited basis.

However, KYC can be also useful for businesses that aren’t subject to AML regulations, such as marketplaces and carsharing platforms. It can help filter out suspicious individuals as well as risky suppliers and platforms.

Click on the links to learn more about KYC compliance by industry.

- Know Your Customer in banking

- fintech

- forex (binary options)

- crypto (defi, NFT, token sales and ICOs)

- real estate

- art dealership

- casinos and betting

- electronic payments

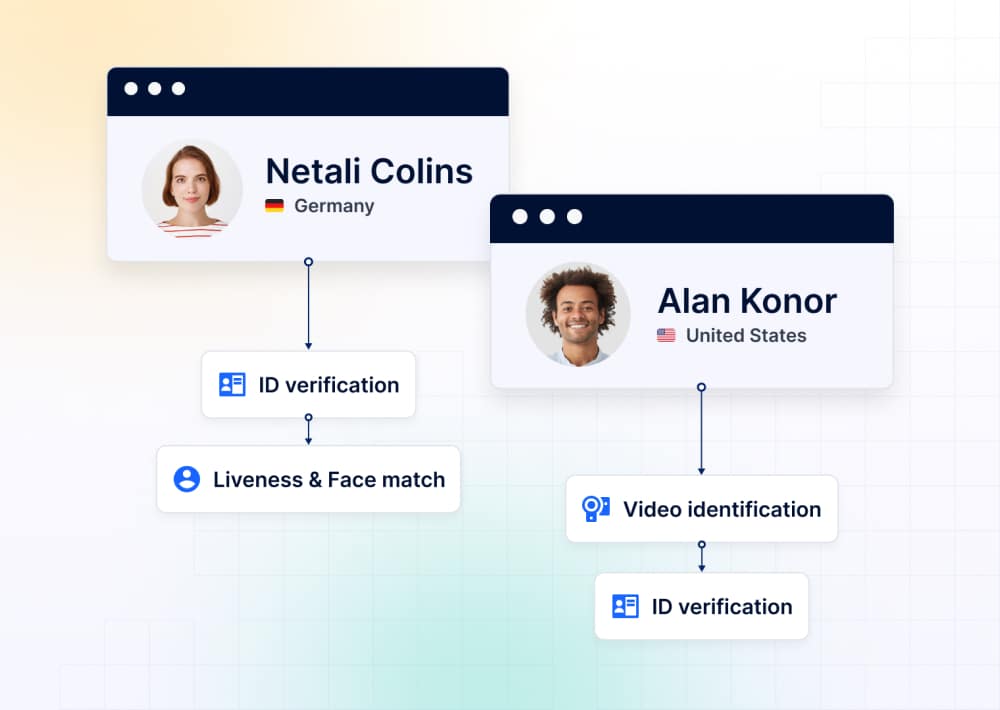

KYC requirements differ across jurisdictions. For instance, Germany demands businesses to conduct video interviews with their customers

KYC requirements around the globe

While many jurisdictions have similar requirements for identifying and verifying customers, the exact list of mandatory KYC checks may differ. In Germany, for instance, businesses must conduct video interviews with customers in addition to document-based verification. Meanwhile in the UK and many other jurisdictions, there’s no such requirement.

Learn about AML requirements and building KYC processes in the following jurisdictions:

Know Your Customer is an umbrella term for everything that a business should know about a customer

Customer Due Diligence and KYC

Customer Due Diligence (CDD) is a set of checks performed by companies when establishing a relationship with a customer or when an existing customer carries out an occasional transaction. This is part of the AML procedures prescribed by local regulations.

CDD and KYC often get confused. “Customer Due Diligence” is a specific legal term that applies to all regulations, while the meaning of “Know Your Customer” can slightly differ from jurisdiction to jurisdiction. In other words, CDD involves a specific list of procedures set by law, while the list of required KYC checks may vary.

- Customer Due Diligence (CDD): The Process and Its Types

- Enhanced Due Diligence: Guidelines and Checklist

Key KYC process steps

KYC checks

The purpose of the KYC procedure is to verify that a customer is who they say they are. Here’s an example of proper KYC steps, in order:

- Identification—requesting that the customer provides their personal data (name, date of birth, address).

- Liveness check—verifying that the customer is a real and living person. This can be done through facial biometrics authentication.

- Verification—checking that the customer is who they say they are. This includes determining that the customer’s documents are authentic and current. This step may include AML screening to check whether the customer is absent in adverse media, sanctions lists, PEP lists, etc.

- Address verification—verifying that the customer actually resides in their selected country by checking utility bills, bank statements, or other proof of address documents. This includes checking whether the customer comes from high-risk countries (Iran and North Korea) or countries under increased monitoring.

- Risk scoring—determining the risk category of the customer based on the results of the above checks. Depending on the calculated risk level, businesses adjust their approach to the customer’s verification. Accordingly, a higher risk score will necessitate additional checks.

However, KYC checks don’t end after the onboarding stage. Under AML regulations, businesses are obliged to continue monitoring a customer’s profile and transactions. This includes checking that documents haven’t expired and detecting suspicious transactions.

- How to Pass KYC

- KYC Checks: Policy and Risk-based Approach to Know Your Customer

- Sumsub Mobile SDK: Fast Customer Verification That Works Right in Your App

- Background Video for KYC: Is It Worth Using?

- NFC Chips and How You Can Use Them For Identity Verification

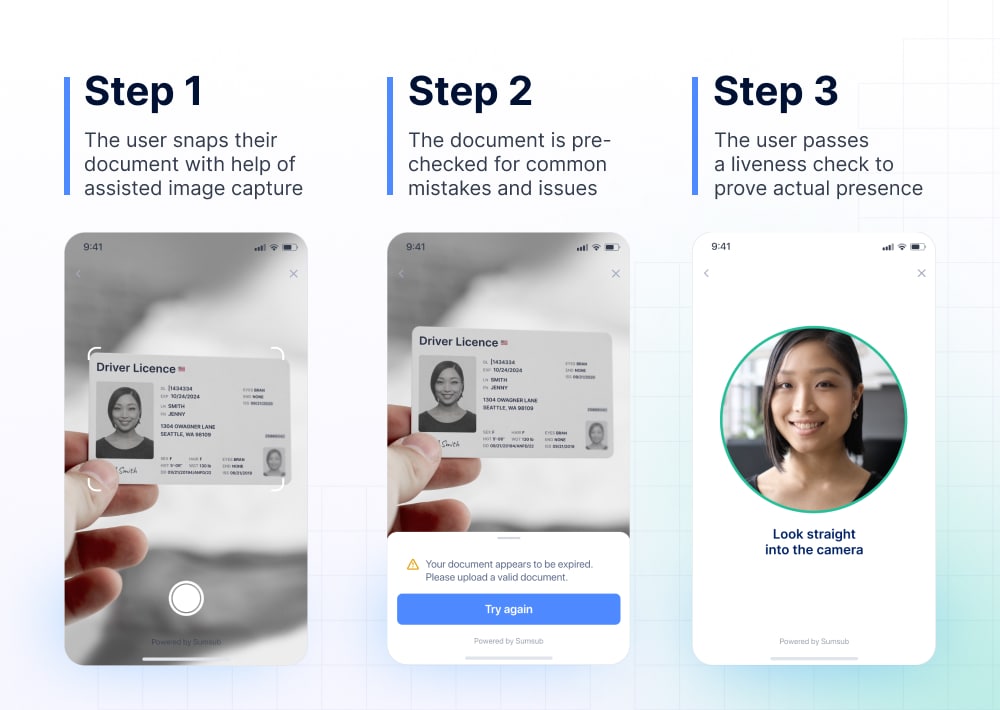

Example of a secure yet user-friendly automated workflow (document screening + facial biometrics check)

What’s eKYC?

Automated KYC solutions, or eKYC, can process documents by extracting their data, checking security features, and comparing them against templates. Algorithms draw together the results of these checks and indicate whether the identity document is authentic.

There are many benefits to switching from manual checks to an automated KYC solution. Automating the process means leaving less room for human error, reducing manual labor, and bringing down associated costs by up to 43%.

- Building Automated KYC: Sumsub’s Insights into Effective Customer Onboarding

- How INGOT Brokers reduced customer onboarding time from 3 days to 3 minutes

How to choose a KYC provider

Different providers offer different KYC services. Some perform AML screening and customer verification while others offer facial biometrics and corporate verification.

The best advice is to choose one solution that covers all the KYC needs of the business, rather than using a combination of different solutions. Here’s how one of our clients puts it:

“The KYC provider we used previously didn’t offer all of the features that we needed, so we had to use a combination of different solutions. Managing everything on multiple platforms wasn’t comfortable, and it was keeping us from launching new products. Therefore, we decided to switch to a single solution that handles all of our requirements and makes the entire KYC and AML compliance process more effective.”—says Andrei Ialama, COO at Paybis.

Here’s the key criteria for choosing a KYC provider:

Compliance. The solution must be compliant with the regulatory requirements of the business’s jurisdiction(s). So, if the business is registered in Austria, its KYC provider must be able to conduct video interviews in accordance with Austrian regulations.

Fraud prevention. Providers should offer strong anti-fraud protection that detects forgeries, spoofing, and other malicious activity.

Flexibility. Businesses should be able to create customizable verification flows for different products and customers.

Coverage. This means support for document types from different countries.

Language support. The solution should have different languages for its interface, as well as OCR (Optical Character Recognition) technology that can recognize non-Latin characters, such as Chinese, Japanese, or Cyrillic scripts.

Speed. The solution should have short processing times and high verification speed, so users won’t need to wait long before being verified.

Welcome more verified users worldwide with Sumsub’s authentic KYC solution. Request a demo today.

FAQ

Frequently Asked Questions about KYC

-

What does KYC stand for?

KYC stands for Know Your Customer, which is the process of identifying and verifying customers.

-

What is KYC and KYS?

Know Your Customer (KYC) is the process of identifying and verifying customers. It can also include additional checks to further monitor customer behavior. Similarly, KYS (Know Your Supplier) is the process of understanding suppliers and business partners.

-

What does a KYC check involve?

KYC checks involve identifying and verifying a customer. They can also include liveness checks, address verification, risk scoring, and ongoing monitoring of the customer’s behavior.

-

Is KYC a part of compliance?

KYC, legally referred to as Customer Due Diligence (CDD), is a key part of Anti-Money Laundering (AML) compliance.

-

What is the first stage of the KYC process?

The first stage is identification of the customer. This involves requesting that the customer provides their personal data (name, date of birth, address).

-

Is KYC a credit check?

The first stage is identification of the customer. This involves requesting that the customer provides their personal data (name, date of birth, address).

-

How do banks conduct KYC?

Previously, banks verified the customer’s identity in face-to-face formats only—which meant that employees had to physically inspect documents. Nowadays, banks can opt for non-face-to-face, automated verification, which is usually faster and more accurate.

-

When was KYC started?

The Financial Action Task Force (FATF), an organization that fights money laundering, was established in 1989. In 1990, the FATF issued a report containing a set of Forty Recommendations, which outlined identity verification (KYC) requirements.

-

What is a KYC questionnaire?

To better know their customers, some businesses request their customers to fill out KYC questionnaires. Such questionnaires can contain questions about sources of funds, planned monthly turnover, relatives, etc.

-

What are the RBI guidelines on KYC?

Reserve Bank of India (RBI) requires banks to identify their customers and provides guidelines on how to do it. We’ll continue to update this article to answer emerging KYC-related questions. Subscribe to Sumsub’s newsletter so you don’t miss future updates. The form is down below.